Scott Kingsley, Senior Wealth Advisor

Pretty much the hardest part of investing isn’t actually picking good investments (though it’s still important, and not easy) – it’s the psychological side. In turbulent markets like we’ve had recently, resolve is tested.

“Is my strategy right?”

“Do I take money out?”

“Is now a good time to invest?”

The last two are matters of timing and, crucially, how you feel about timing.

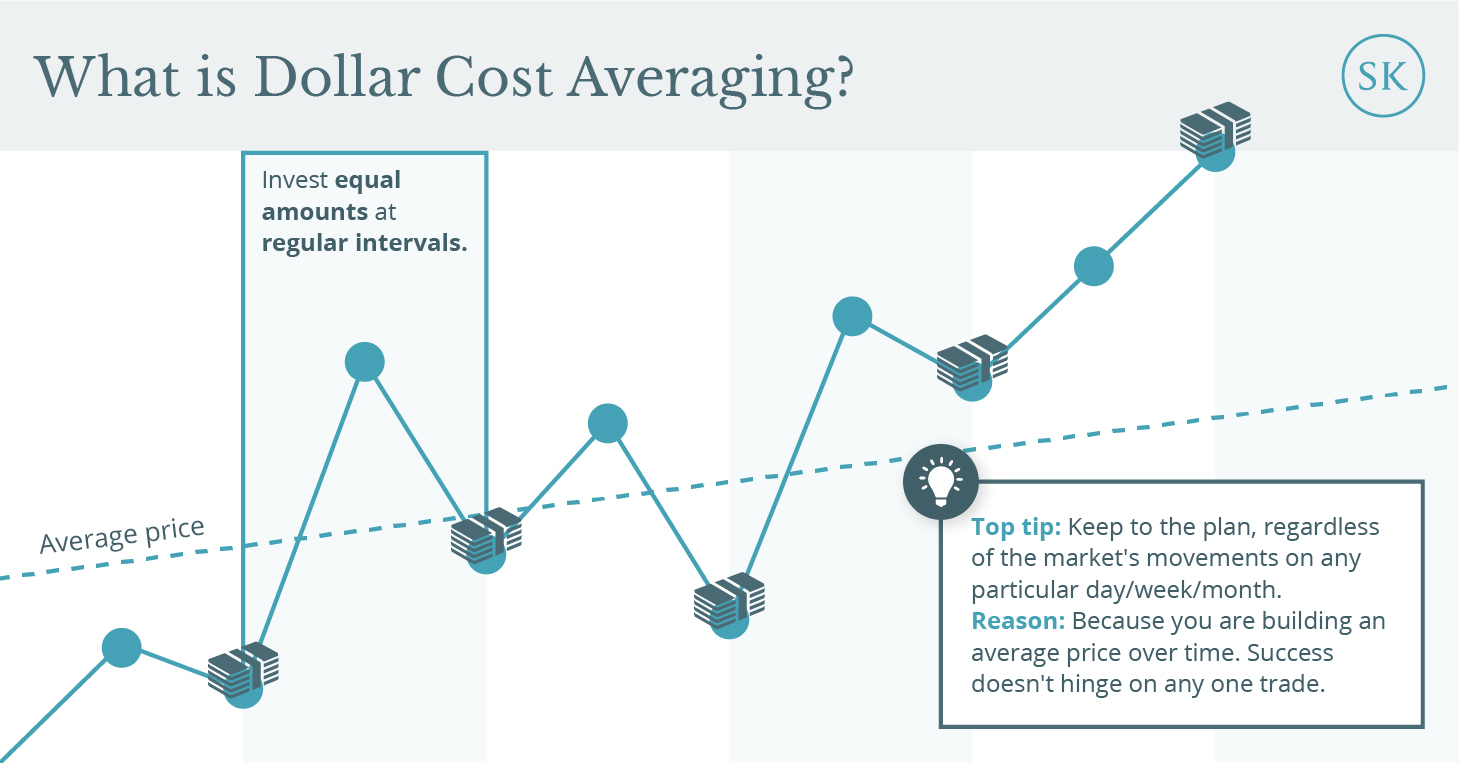

There is one strategy which nullifies this factor and is therefore an attractive approach for the majority of private investors – Dollar cost averaging.

It’s the alternative to investing all in one go. You commit to investing smaller, equal sums at regular intervals. It means you buy fewer units at higher valuations and, therefore, prices and, crucially, more units when valuations are lower, and prices are down. It also means you don’t worry anywhere near as much about timing or market levels which is much, much less stressful.

Therefore, it is a solid strategy for a bear market, or in recessionary periods. The simple truth is that, whilst we know markets move in cycles, no one knows how long they will be, so if your time horizon is a decade or more then you will have all manner of economic conditions to contend with.

Interestingly, you may actually already be Dollar coast averaging but unaware of it.

Your workplace retirement scheme will generally take contributions from your monthly salary, investing it into some form of stock market portfolio. This can be psychologically very different, of course, because (caution: generalisation incoming) people are more passive about their work scheme than they are their private investments, or any retirement pots they pay into privately. Apart from those approaching retirement day, of course. But it still works in the same way, insulating your capital against the risk of investing one large sum at, or near, a market peak. Trying to time the market once is difficult; doing it repeatedly is beyond the vast majority of even professional money managers, especially over long time periods, a decade or more and the investments you make in the tough times will be the best ones you ever make. Is it worth, then, considering a regular investment strategy?

In most cases, yes, it has merit. There are disadvantages though.

If you have a pot of cash which you’re drip-feeding into the markets you’re going to be holding cash for longer than you would if investing in one bite. But, of course, up to a point, well, holding cash for longer is the point!

If markets are in a general uptrend you’re not participating in that rise as much as you might otherwise have; however, if markets are falling, you’re feeling pretty smug as you pick up ever more shares for your set amount.

That said, even as interest rates on cash creep up, they still lag inflation in most places, so your side-lined cash is losing purchasing power.

But given how wildly stock indices can swing, the capital saved by avoiding a downward leg in markets and sticking to a regular monthly investment amount can often outweigh the bite inflation takes out of your money while you watch it happen from safety of the touchline.

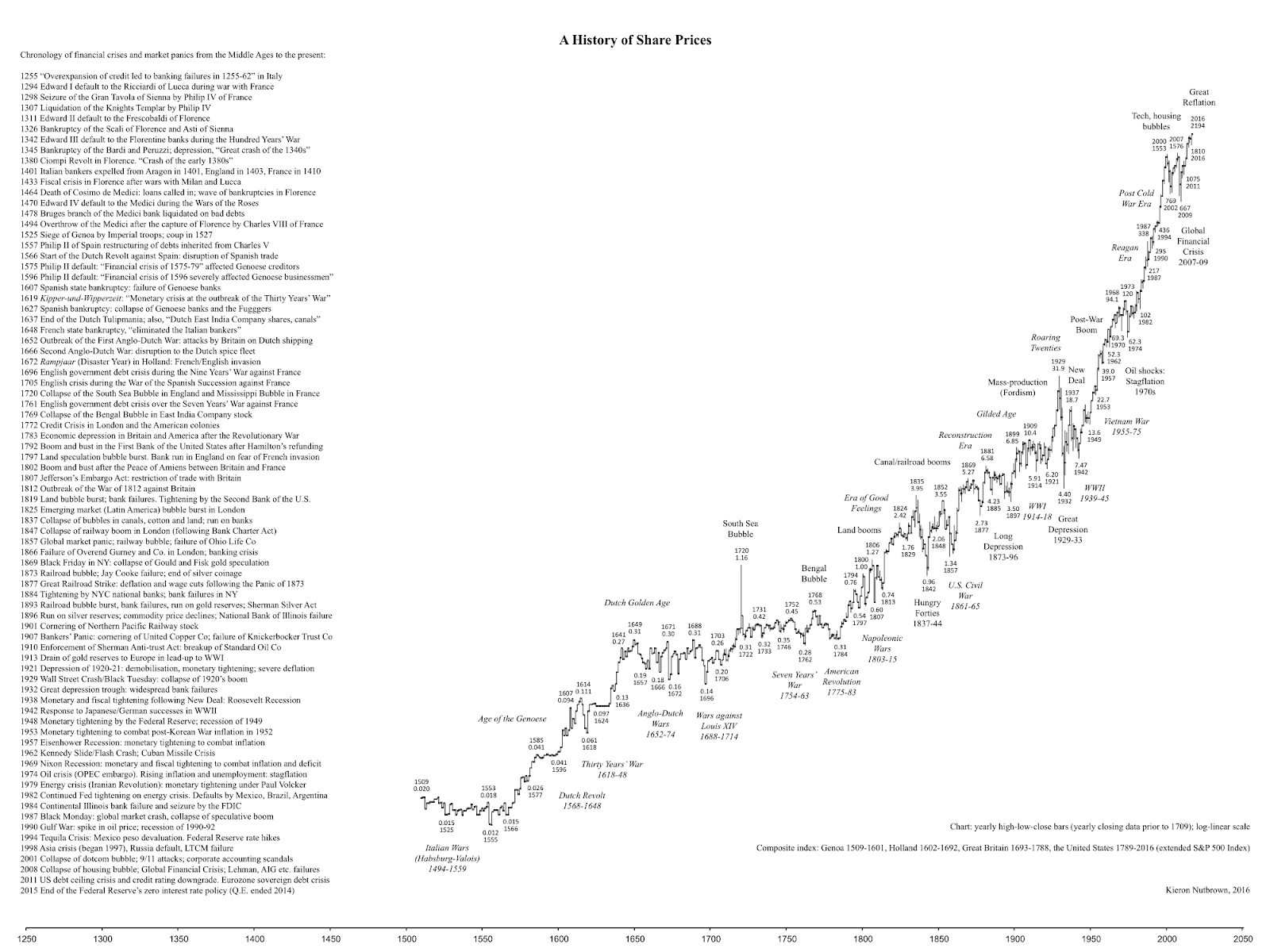

What isn’t in any doubt, though, is the veracity of long-term stock market investing as a means of preserving and creating wealth, as this chart so astoundingly shows:

It’s as clear an illustration imaginable of the ability of markets to shrug off events that seem, often are, catastrophic at the time. So, the basic premise for any sound investment strategy is a long-term outlook and a willingness to stick out the tough times. That holds whether you’re a lump sum kind of a person, or more little-and-often.

Which fork you take depends on a few things. Mentality being at the forefront. The more cautious investor may be more likely to prefer dripping funds in. Perhaps also the investor who wants to get into the habit of investing. And anyone prone to serious cases of investment FOMO would always like to have a little dry powder to take advantage of the next big thing. Yet you can have cautious lump sum investors; and aggressive regulars.

As with so much in life, it is about personality and preference but, if everyone were to Dollar cost average, instances of investment regret would be very few and far between, and the journey would be less stressful.

If you’d like to discuss this article in more detail or to find out more about how our member, Scott Kingsley can support you with your financial goals, please feel free to get in touch - it won’t cost you anything to speak to him, or, alternatively, head over to his website to find out more about the services.